Are you tired of reaching the end of every month with nothing left in your account? You’re not alone. Millions of people live paycheck to paycheck — not because they don’t earn enough, but because no one ever taught them the right saving money habits.

The truth is, most people fail at saving money because they treat it as an afterthought. They spend first, plan to save “whatever’s left,” and wonder why nothing ever changes. The problem isn’t willpower — it’s the absence of a system.

The good news? You don’t need a six-figure salary to build financial security. You need the right daily habits. In this guide, you’ll discover 7 powerful money habits, along with practical saving money tips, that can genuinely transform your financial life and help you start saving money — no matter where you’re starting from.

Why Is Saving Money Important?

Before diving into the habits, it’s worth understanding exactly why saving money matters — because motivation is the foundation of lasting change.

Financial security and stress reduction.

When you have money saved, you’re not one unexpected expense away from a crisis. A car breakdown, a medical bill, or a job loss stops being catastrophic and becomes manageable. This is why saving money matters — applying practical saving money tips and building strong money habits helps reduce financial stress, one of the leading causes of anxiety and relationship problems.

Freedom to handle emergencies.

Life is unpredictable. An emergency fund means you can handle surprises without going into debt or borrowing from family. This freedom is priceless.

Opportunity to invest and grow wealth.

Savings aren’t just money sitting idle — they’re the raw material for wealth-building. Once you have a financial cushion, you can begin investing, which allows your money to grow through compound interest over time.

Ability to achieve life goals.

Whether it’s buying a home, starting a business, funding your child’s education, or traveling the world — every major life goal has a financial component. Consistent saving is what makes those dreams achievable.

Independence and retirement planning.

The earlier you save, the more choices you’ll have later. Saving for retirement in your 20s and 30s means you won’t be forced to work into your 70s. Financial independence gives you the ultimate freedom — the ability to choose how you spend your time.

How to Start Saving Money

If you’ve never really saved before, the concept can feel overwhelming. But starting is simpler than you think. Here’s a beginner-friendly, step-by-step approach to get the ball rolling.

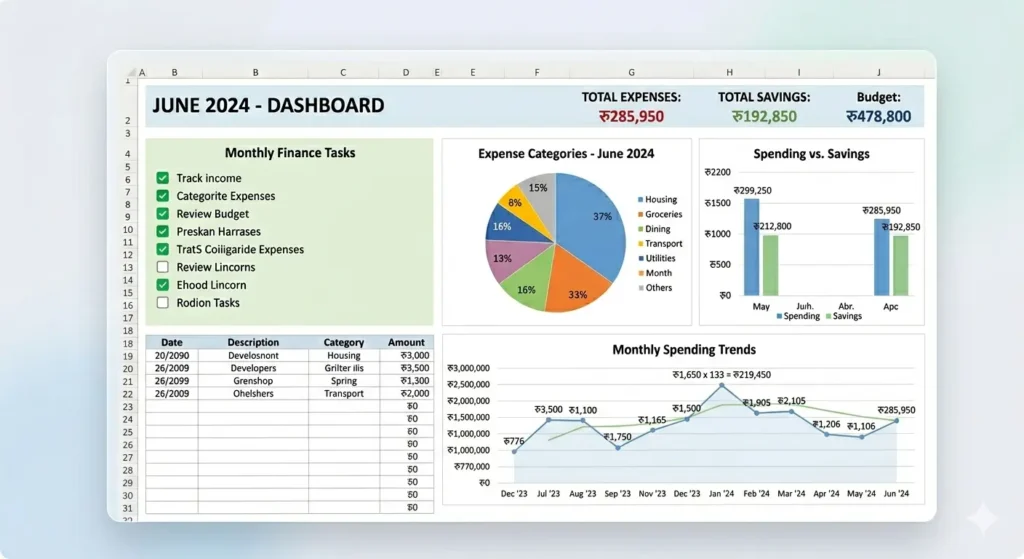

- Track your progress monthly. At the end of each month, review your budget and savings balance. Celebrate small wins. Adjust what isn’t working. Progress — even slow progress — builds momentum.

- Know your income and expenses. You can’t control what you can’t see. Start by writing down exactly how much money comes in each month and where every dollar or rupee goes. Most people are surprised — and a little shocked — by what they discover.

- Create a basic budget. A budget isn’t a punishment — it’s a plan. Allocate your income toward needs, wants, and savings money starts before the month begins. The popular 50/30/20 rule is a great starting point: 50% for needs, 30% for wants, and 20% for savings.

- Start small (even 5-10%). You don’t need to save 30% of your income right away. Even saving 5% is infinitely better than saving nothing. The key is to start, build the habit, and increase gradually.

- Automate your savings. Set up an automatic transfer to a separate savings account on payday. When saving happens automatically, you remove the temptation to spend that money first.

Saving Money Challenges (And How to Beat Them)

Knowing you should save and actually doing it are two different things. Here are the most common obstacles people face when saving money — and practical solutions for each, Some saving money tips are listed below which you can apply in your personal finance.

- Lack of financial education — Reading and applying guides like this one is how you close the knowledge gap.

- Low income — Even saving NPR 2000-5000 a month builds the habit and adds up over time. The habit matters more than the amount when you’re starting out.

- Lifestyle inflation — As income increases, spending tends to increase too. The fix is intentional living — deciding in advance how much of any raise or bonus you’ll save versus spend.

- Impulse spending — Emotional buying is one of the biggest leaks in any budget. Awareness is the first step; structured rules like the 24-hour purchase rule are the cure.

- Debt pressure — Tackle debt aggressively while saving a small emergency fund simultaneously, so you don’t keep adding new debt when surprises arise.

Saving Money Tips That Can Change Your Life

Pay Yourself First

Most people save whatever is left after spending. The “pay yourself first” approach flips that entirely — you save a set amount the moment your paycheck arrives, and you live on the rest.

This works because it removes saving from the realm of willpower. You’re not relying on yourself to resist spending temptations all month; the money is already gone into savings before you even see it.

Set up an automatic transfer to a dedicated savings account on payday. Aim for at least 20% of your income if possible — but start with whatever is realistic. Even 5% is a powerful beginning.

Why does this work psychologically? Because humans adapt to their available resources. If you consistently receive only 80% of your paycheck in your spending account, you naturally adjust your lifestyle to that amount.

Track Every Expense

You cannot manage what you do not measure. Tracking every expense — even small ones like coffee or a quick snack — creates a level of financial awareness that is genuinely transformative.

Awareness equals control. When you see exactly where your money is going, patterns become obvious. You might discover you’re spending Npr 3000 a month on food delivery without realizing it, or that multiple forgotten subscriptions are quietly draining your account.

Use apps like Karobar, (GHK) Gharayasi Hisab Khata, or even a simple spreadsheet to log expenses. Set up a monthly review — 15 minutes at the end of each month to look at your spending by category:

- Housing

- Food & dining

- Transport

- Entertainment & subscriptions

- Personal care

Live Below Your Means

One of the most powerful and most overlooked personal finance habits is simply spending less than you earn. Not dramatically less. Just consistently less.

The key distinction is between needs and wants. Needs are things required for survival and basic functioning: housing, food, utilities, transportation to work. Wants are everything else.

Beware of lifestyle inflation. Every time income increases, there’s a natural pull to upgrade your lifestyle — a nicer car, a bigger apartment, more frequent dining out. This is normal, but it’s also how people end up earning twice as much while feeling no more financially secure.

- Practical downsizing ideas:

- Delay non-essential purchases for 30 days to see if the desire passes

- Cook at home more often

- Choose entertainment that doesn’t require spending

- Shop secondhand when possible

Build an Emergency Fund

An emergency fund is non-negotiable. It is the single most important financial safety net you can build — and without it, every unexpected expense threatens to derail your finances entirely.

The standard recommendation is to save three to six months of living expenses. This sounds like a lot, but you build it gradually. Start with a goal of Npr 50,000-1,00,000 as your “starter” emergency fund, then build from there.

Where to keep it: a high-yield savings account, separate from your everyday checking account. Keeping it separate reduces the temptation to dip into it.

- Build it step by step:

- Once you reach your target, redirect those contributions to investments

- Set a monthly contribution — even Npr 5,000 a month adds up to Npr 60,000 in a year

- Automate the transfer so it happens without effort

Avoid Bad Debt

Not all debt is created equal. Understanding the difference between good and bad debt is essential to building long-term financial health.

Good debt is borrowing that helps you build wealth or income over time — a mortgage, a student loan that increases your earning potential, or a business loan. Bad debt is borrowing to fund consumption — credit card balances, personal loans for vacations, or financing depreciating items.

If you’re in bad debt, use one of two proven payoff strategies:

The Snowball Method

Pay minimum payments on all debts, then throw all extra money at the smallest balance first. When it’s cleared, roll that payment into the next smallest. This builds psychological momentum through quick wins.

The Avalanche Method

Pay minimums on all debts, then focus extra payments on the highest-interest debt first. This saves the most money in interest over time.

Invest Consistently

Saving and investing are not the same thing — and understanding the difference is crucial.

Saving money is keeping money safe and accessible for short-term needs and emergencies. Investing is putting money to work in assets that grow over time — stocks, bonds, index funds, real estate — with the goal of building long-term wealth.

The most powerful force in investing is compound interest. When your investments earn returns, those returns earn returns — and over decades, this creates exponential growth.

For beginners, the best investment options are simple:

- Diversified index funds tracking the stock market

- A PF ,SSF for retirement savings

- A robo-advisor that manages a portfolio automatically based on your goals

Start small. Even Npr 5,000 a month invested consistently is better than waiting until you can invest Npr 50,0000. The habit matters more than the amount.

Set Clear Financial Goals

Saving without a goal is like driving without a destination. Goals give your money habits meaning — and they dramatically improve your consistency and motivation.

Use the SMART framework for setting financial goals:

- Specific — “Save Npr 50,000 for an emergency fund” rather than “save more money”

- Measurable — Track your progress with a number

- Achievable — Set goals that challenge you but are realistic given your income

- Relevant — Goals should connect to your actual values and life priorities

- Time-bound — Set a deadline to give your goal urgency

Track your goals visually — a savings thermometer, a spreadsheet, or a goal-tracking app. Seeing your progress creates motivation to continue.

How to Save Money Fast (Action Plan)

Sometimes you need results quickly. These quick wins can meaningfully boost your savings in days or weeks.

- Cancel unused subscriptions — Go through your bank and credit card statements right now. Cancel anything you haven’t used in the last 30 days.

- Follow the 24-hour purchase rule — Before buying anything non-essential, wait 24 hours. Most impulse urges fade completely.

- Cook more at home — Cooking just 3 extra meals at home per week can easily save Npr 15,000-30,000 a month.

- Negotiate your bills — Call your internet provider, insurance company, and phone carrier. Ask for loyalty discounts. This takes 30 minutes and can save hundreds annually.

- Sell unused items — List anything you haven’t used in the past year on Facebook Marketplace or eBay for an instant cash injection.

- Use the 50/30/20 rule — 50% for needs, 30% for wants, and 20% directly to savings.

Monthly Money Habit Checklist

Use this checklist at the end of each month to stay on track with your personal finance habits:

- Review your monthly budget — did spending match the plan?

- Transfer your savings — confirm the automated transfer went through

- Track all expenses by category and identify any surprises

- Review your debt balances — are they going down?

- Check progress toward your financial goals — are you on track?

- Cancel any subscriptions you didn’t use this month

- Review investments — no need to make changes, just stay informed

- Celebrate any wins, no matter how small

Running through this checklist takes 15-20 minutes but keeps your entire financial life moving in the right direction month after month.

Final Thoughts: Small Habits Create Big Wealth

Wealth is rarely built through a single dramatic decision. It’s built through the quiet, consistent repetition of simple habits — saving money before spending, tracking where your money goes, investing a little each month, and keeping your spending in check even when your income grows.

You don’t need to be perfect. You don’t need to start with a large amount. You just need to start.

Pick one habit from this list — just one — and implement it this week using these saving money tips and strong money habits. Then add another next month. Within a year, your financial life will look dramatically different from where it stands today.

What is the best way to start saving money?

Start by creating a simple budget, automating a savings transfer on payday, and tracking your expenses consistently. These three steps alone will put you ahead of most people.

How much money should I save monthly?

Aim for at least 20% of your income as a long-term goal. But start with whatever you can manage — even 5% builds the habit. Increase the percentage as your income grows or expenses decrease.

Why is saving money hard?

Lifestyle inflation, debt pressure, impulse spending, and lack of a clear plan make saving difficult for most people. The solution is building automated systems that remove the need for constant willpower.

How long does it take to build good money habits?

Research suggests most habits solidify within 60-90 days of consistent practice. Start small, stay consistent, and give yourself grace during the learning period.

Leave a Reply